")

")

What is the starting position? There is a lot to choose from, and many biotech ideas are seeking investors. Unfortunately, a certain chicken-and-egg situation prevails, especially in Germany: Supposedly there are no success stories, but these cannot develop due to a lack of financial resources. Yet capital is available in abundance and is looking for investment opportunities. Unfavorable government regulations for high-tech investments of the financial sector, low risk appetite as well as bad experiences respectively lack of biotech know-how among investors characterize the situation in this country for biotech financing. Nevertheless, the recent pandemic has brought the biotech sector a great deal of increased attention. Individual "unicorns" (such as BioNTech and CureVac) together with their daring private investors (Strüngmann and Hopp) have shown that biotech investments are also worthwhile in this country.

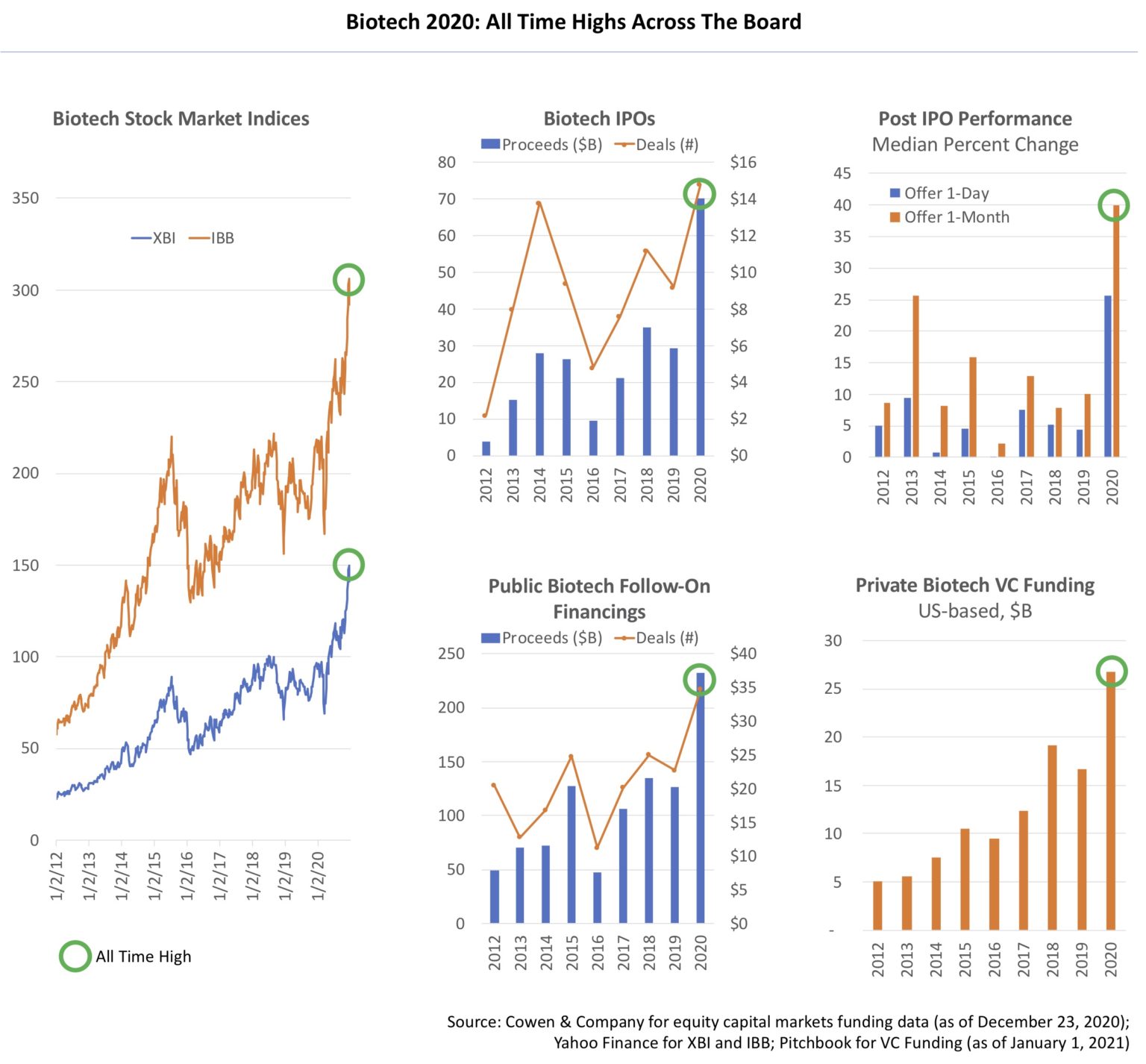

When it comes to financing, the industry always looks reverently to the U.S. There, for the first time almost US$100 billion in fresh capital flowed into biotech in 2020. A so-called "all-time high", a "magic threshold" based on a close doubling of the previous year's figure. And, mainly driven by follow-on financing of already listed companies, be it equity or debt. This data comes from EY's latest German Biotechnology Report.

This is a strength of the U.S. biotech industry, the presence of many public companies. Twenty years after the "founding" of the industry there, that is, in the mid-1990s, there were already around 300 such firms. EY's latest Global Biotechnology Report, published in 2017, counted nearly 450 public companies in 2016.

Today, there are estimated to be at least 500 companies, as there have been more than 150 IPOs of U.S. biotech firms in the last four years. Bankruptcies or acquisitions also occur from time to time in the U.S. industry, so there are also exits in the statistics. More than 250 companies are listed in the NASDAQ Biotech Index (NBI): Requirement of at least US$200 million market value. However, there are also some non-US companies on the NASDAQ.

Other sources, other numbers, but the latest look from Cowen & Company confirms the data from EY, which has the most restrictive definition of what a biotech company is of any provider. Presumably, that's why the investment bank's numbers are higher. Their look at the post-IPO performance impressively shows what the past year has brought in terms of share price development: On the first day as well as in the first month after the initial public offering (IPO), a share price increase of 25% and 40% on average.

Certainly, the pandemic has had a major impact, and awareness of biotech has increased tremendously. However, biotech has also brought REAL progress, as biosciences have been brought into marketable application at a rapid pace, in the form of novel and highly effective vaccines.

Delivered by mRNA technology providers BioNTech and CureVac, both from Germany, as well as ModeRNA from the US. The latter raised US$1.34 billion in May 2020 via the issuance of additional shares on the stock market. Also unmatched is their record biotech IPO in 2018 of US$604 million.

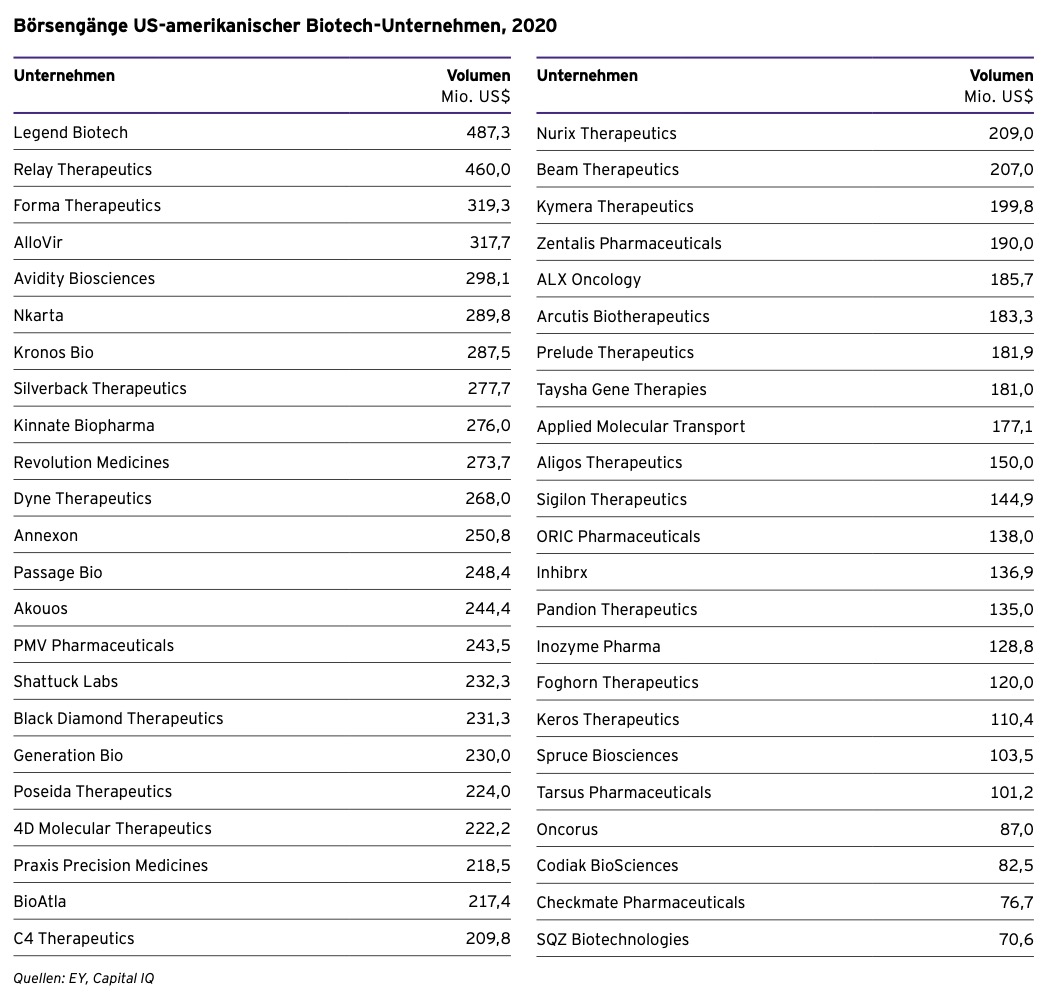

The average IPO size in 2020 for U.S. biotechs was just over US$200 million. After all, CureVac from Tübingen was able to achieve the same size last August. One of the largest IPOs of a German biotech company! BioNTech raised US$150 million in its IPO in October 2019. However, both companies were only able to achieve such amounts on the U.S. stock market, which would have been unthinkable in this country. The argument often used is: lack of peer groups, liquidity and analysts.

Compared with biotech financing in the U.S., that in Europe has been much lower for years: Only about one-fifth of the U.S. amount is achieved. However, the European biotech sector is also 10 to 15 years younger than that in the U.S. A direct comparison is therefore not very meaningful; basically, the age difference would have to be priced in. The generally smaller number of financing rounds in Europe also results in a smaller sum. And finally, the number of listed companies is smaller by at least a factor of 50%.

However, a look at average financing amounts shows the clear supremacy of the U.S. They are about twice as high for venture capital and 50% to 100% higher for IPOs. The reasons for this are certainly the mature and very well functioning capital market ecosystem, biotech experience and investor confidence, and early biotech success stories as role models.

After all, European biotech financing has been rising steadily over the past 10 years. This is particularly evident in follow-on funding of listed companies and venture capital. For IPOs, it is not so clear at first glance, but the average amount reaches an all-time high of €122 million due to strong growth (34% annual growth rate).

In Europe, the number of large venture capital rounds (>€100 mln) is higher than ever before. This is a positive development and gives hope that investors will also gain more confidence in the European biotech scene.

By comparison, in the U.S., seven transactions in 2020 were worth more than US$200 million. The two largest rounds were raised by Sana Biotechnology in a pre-IPO venture capital round (US$700 mln) and Lyell Immunopharma with almost US$500 million. Both companies are developing innovations in cell and gene therapy. Sana succeeded in an IPO in February 2021 valued at almost US$600 million, an absolute record for a preclinical biotech company.

In terms of totals, the UK is more or less always ahead in European venture capital investments. Biotech companies there may have a longer history of established relationships with Anglo-Saxon investors. Germany moved up into a comparable league in 2020 due to the "exceptional funding" at CureVac. The years before, the financing amounts were more on par with companies from France and Switzerland.

Biotech financing in Germany: Is the "problem child" of recent years now getting on a promising path? The first biotech hype in 2000 left behind a lot of "scorched earth" and the German biotech scene languished for over a decade due to a lack of investment. Many projects were chronically underfunded, the aforementioned chicken-and-egg situation. At the time of the hype, most of the firms were still very young, the investors inexperienced - in contrast to the U.S.

For about five years now, the situation has been increasingly recovering and investors are regaining confidence in the German scene, which has a lot to offer. From a scientific point of view, German biotech research and development does not have to hide as our current "pandemic saviors" show!

From 2004 onwards, private investors regularly accompanied the German biotech sector in financial terms: investments by German family offices supplemented those of classic venture funds. From 2008 to 2015, private direct investments saved the local scene through a long and cold financing winter. In some years, their investments accounted for 70% to 80% of total venture capital.

This was mainly thanks to the Hopp and Strüngmann families, who reinvested money generated from their own entrepreneurship. In addition, MIG AG financed, which invest money from private investors. As is well known, they have all recently been rewarded for this: product successes and stock market exits of their investments CureVac and BioNTech are familiar to almost everyone today.

Another "horse from this stable" is Tübingen-based Immatics, which realized a SPAC IPO of €224 million on NASDAQ in 2020.

It was not until 2016 that classic VC investors - especially those from abroad - returned in greater numbers. In addition, corporate venture funds invested. This, after all, provided German venture capital financing with annual growth of over 20%.

An additional special chapter for German biotech companies are IPOs. After a dozen German biotechs went public on the Neuer Markt (segment of the Frankfurt Stock Exchange) around the first biotech hype, another dozen took advantage of this opportunity in the years 2004 to 2007, even though the Neuer Markt segment itself no longer existed. After that, the Frankfurt Stock Exchange window closed for a long time until February 2016, when BRAIN Biotech raised about €30 million via IPO. This is a company in the white biotech segment. No other company in the red biotech segment has gone public in Germany since then. One exception is biosimilar specialist Formycon, which has been on the Frankfurt Stock Exchange since 2010 via a listing of Formycon's predecessor Nanohale. Further listings or "real" IPOs have taken place either on another European stock exchange or directly in the USA on the NASDAQ.

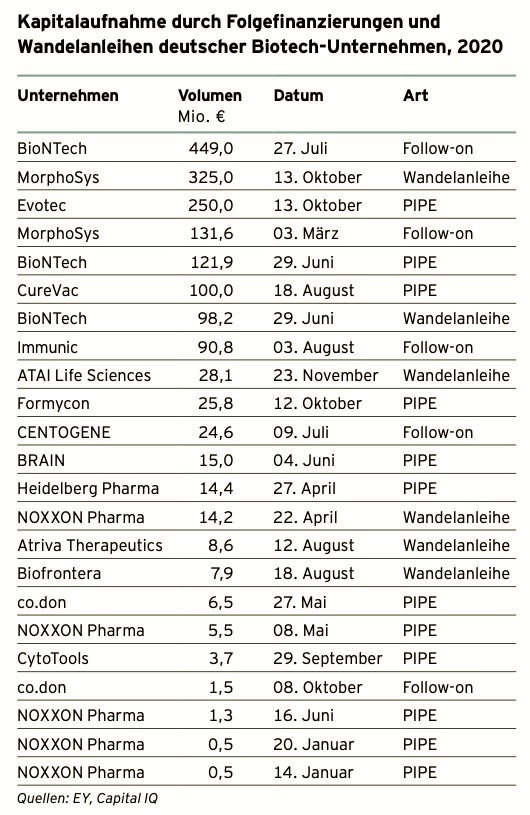

However, the listing itself (so to speak no matter where) is a good basis for follow-up financing based on the issue of further shares. Be it as a public offering via the stock exchange (follow-on) or as a PIPE (private equity in public entities) to a closed private circle. 2020 brought an explosion in financing amounts, perhaps also due to the pandemic. At the forefront were either the German biotech veterans Evotec and MorphoSys or the stock market newcomers BioNTech and CureVac. All amounts larger than 50 to 100 million euros are right rarities of German biotech financing.

Increasingly, convertible bonds are also being used as an instrument of biotech financing, i.e. bonds that can be exchanged for shares. This financing option is now also being used by unlisted companies. So far, only large U.S. biotech companies have taken out pure loans.

With a total of three billion euros in capital proceeds in 2020, the German biotech industry is better financed than ever before. It is to be hoped that further investors can discover the great potential for themselves in order to support an industry which, due to recent developments, can almost be described as systemically important.

There are estimated to be more than 6,000 biotech companies worldwide. Other sources list well over 10,000 companies. As always, the definiton of biotech is decisive for counting. Startups looking for capital or companies already listed on the stock exchange are of interest as investments. There are professional database providers for both categories, so a range of options or alternatives is available. In addition, there are opportunities to get in at a very early stage and participate directly in spin-offs. Here, the technology transfer offices of the universities are ready to help. Often investors are also looking for co-investors and conferences are held to bring the different parties or players together.

The question is again, how to make the selection, which comparison, selection and decision criteria to use? The basis of every decision is sufficient background knowledge to make meaningful sortings.

Understanding Biotech and Identifying Trends already gives a few hints as to where the biotech journey may lead in the future. The healthcare sector continues to be a very important and rewarding field. Health is simply THE most important commodity, which unfortunately is currently being shown to us relentlessly.

Spending on healthcare in Germany has risen by 3% annually over the last 25 years to over €400 billion in 2019, while in the U.S. the figure was almost US$4,000 billion. These are correspondingly simultaneous markets.

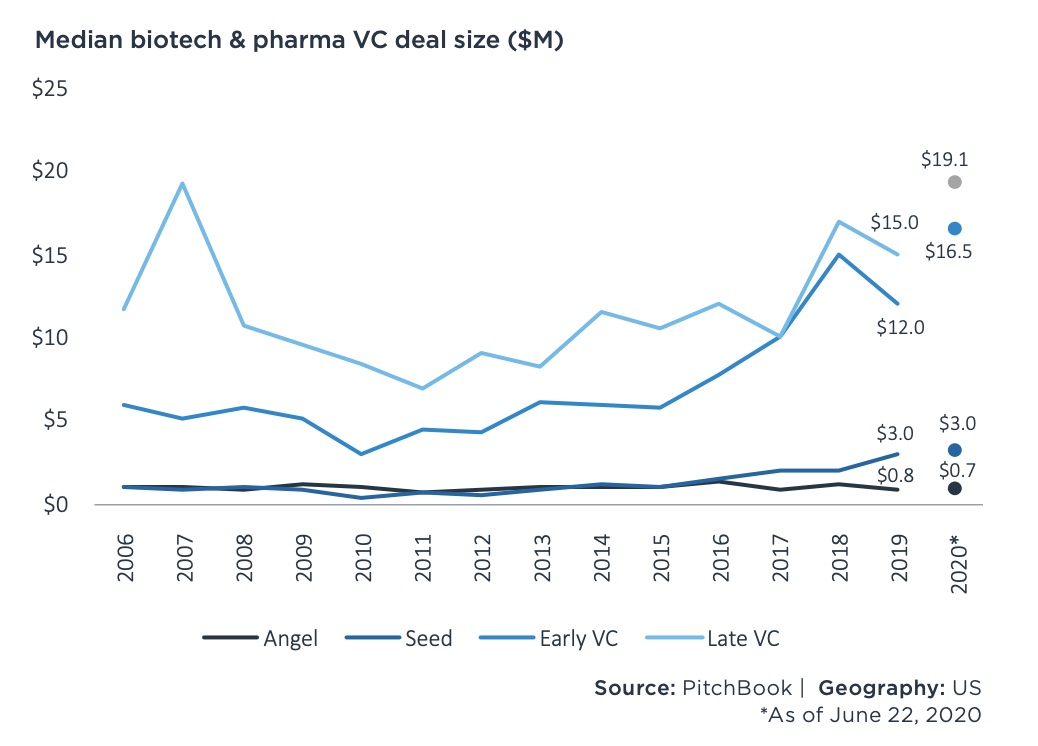

Venture capital funding for biotech and pharma startups has more than tripled in the last decade (2009-2019) from US$5 billion to US$13 billion, according to Pitchbook. The goal is to revolutionize the healthcare system and provide better treatments for patients. In addition to biotech investments, approaches to digital health and artificial intelligence play a major role here.

There are a number of database providers that make biotech options searchable and findable. Some of these are visually very appealing, such as CB Insights. Biotech is only a subset of their "tech market intelligence platform". Alternatives and opportunities can also be found at Crunchbase and Pitchbook, both of which also work across technologies and focus on private companies. The latter is part of Morningstar, a financial information and analysis company.

CipherBio, on the other hand, focuses purely on life sciences and is operated by SVB Financial Group, which includes Silicon Valley Bank (SVB). It is one of the few banks that provides debt financing to high-tech companies and startups. BioCentury and Biotechgate also have a strong biotech focus, both of which see themselves as providers of information and analysis on biotech and life sciences.

The trick, nevertheless, is to understand the difference in the multitude of alternatives, then to determine the "best" option, and finally to gain access.

Know-how from other sectors is hardly transferable because biotech is different from virtually all other sectors due to

Different levels of expertise are certainly required depending on the stage of entry, in part because investment levels can vary widely. For example, in U.S. biotech financings, angel investments are below the US$1 million threshold. Startup investments averaged US$3 million in 2019. Larger venture capital rounds then become the case with corresponding early and late-stage financings, at US$12 million and US$15 million on average.

In the U.S. in particular, there are specialized investors with a great deal of experience in the healthcare sector, especially in biotech and life sciences. Large funds are being set up there, most recently for example by

In Europe, specialized investors with currently larger funds are

In addition to fund companies and venture capitalists, pharmaceutical and chemical companies also invest in the form of corporate venture funds.

It may be of interest to first analyze and access fund investments before considering direct investments.

This information creates trust for cooperation? Connecting options aims to identify relevant players and bring them together. Biotech.Match is the motto behind it. The creation of a kind of meta-company database will make it possible to answer individual questions quickly. My offer to you also includes attending relevant investor conferences and looking for suitable investment opportunities. Let's discuss together how and where to find the jewel, I look forward to hearing from you.